MACROECONOMIC MODELING: There are two different ways to model the economy.

-Bottom up modeling uses all of the principles of microeconomics (such as profit and utility maximization) and analyzes the choices made by workers, firms, consumers, and others to create a model of the economy. A bottom-up model assumes that the economy works, and thus wages and prices are flexible within a bottom-up model.

-Top down modeling is a macroeconomic aggregation (summation) which analyzes the collective behavior of larger groups (as opposed to individual actors). Thus, top down modeling focuses on total demand and supply within an economy, and also assumes wage and price rigidity.

OUR course follows the Top Down approach to macroeconomic modeling. We do not explicitly rely on microeconomic foundations here, and we are initially assuming wage and price rigidity.

REMEMEBER:

-Macroeconomics is concerned with the 'big picture'

-Macroeconomics studies aggregates and how government policy affects them (ie: the government can manipulate the economy)

-The concepts of price and quantity which we learned in Microeconomics now become the general price level (P) and the national income or production or Gross Domestic Product (Y)

-Two issues of major importance are BUSINESS CYCLES and GROWTH of Y

BUSINESS CYCLES: The cycles of the national income in the medium term

GROWTH of Y: The long term trend of national income

Macroeconomics studies FISCAL and MONETARY policy

FISCAL POLICY: Government policies regarding taxation and spending

MONETARY POLICY: Government policies regarding interest rates and the money supply

There are 5 different variables which we have to learn for macroeconomics. Y, U, P, i, & e (we call these the YUPie varaibles in Gateman's class). For each of these different variables, we will be learning what exactly the variable refers to, what historical trends have we observed regarding the variable, and why the variable is important.

-----------------------------------------------

Y: OUTPUT AND INCOME

****REMEMBER: Output generates income!

DEFINITION OF Y: Final market value of all goods and services produced in the economy during a defined period of time (usually a fiscal year).

Final- refers to the fact that intermediate goods do not count towards GPD (so you cannot count both a car and the steel needed to produce that car both as contributors to national income)

Market Value- This refers to the value of products as determined by supply and demand

Good and Services- Both concrete goods (like tomatoes) and immaterial goods (like economics classes) contribute to GDP

Produced in the economy- this refers to the fact that 'flipping' products does not add to the GDP, so a stock broker who makes a small fortune from buying and selling stocks is not technically contributing to the GDP. On the other hand, if this broker were were to create a financial brokerage service for others, this WOULD contribute to the GDP (because the broker could be seen as offering a service to others for money)

A fiscal year in Canada is usually from April of one year until April of the next year, because that is when the government unveils the budget (their plan regarding spending and taxation)

Nation Income (Y) is the 'target' at which we aim the economy- in other words, it is the variable which we seek to manipulate directly in order to make changes to the economy. The government uses fiscal and monetary policy to accomplish this task. Unemployment (U) is inversely related to growth in Y, so as national income grows, unemployment shrinks. Conversely, as the national economy shrinks, unemployment rises. Inflaction (P) is directly related to growth in Y, so as the national income grows, the general price index (aka inflation, aka P) will increase.

Just REMEMEBER THIS:

National income (Y) is the primary target of attempts to manipulate the economy

Unemployment (U) and Inflation (P) are secondary

Interest Rates (i) and Exchange Rates (e) are tertiary

So, in other words, every macroeconomic variable we deal with in this course is affected by national income.

-------------------------------

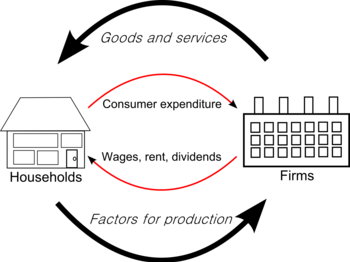

THE CIRCULAR FLOW DIAGRAM

The red arrow flowing from households to producers represents flow of factors (workers provide factors to producers so that consumers may produce products)

The black arrow flowing from producers to households represents flow of income (producers give workers wages in return for providing labour as a factor of production)

The red arrow flowing from producers to households represents flow of output or goods (households buy products from producers)

The black arrow flowing from households to producers represents flow of expenditures (households pay producers money in order to purchase goods)

The red arrows here show real flows (flows of real goods, services, and factors), while the black arrows should money flows. There are two systems represented here: the output-expenditure flow (also known as the products market) and the factor income flow (also known as the factor market)

IMPORTANT*** GDP(Y) = GDP(E) (income = expenditures)

Also, OUTPUT GENERATES INCOME (so the higher our output, the higher out income)

This basic circular flow structure is called a spendthrift economy.

If we add a bank to the system, we can call it a frugal economy. Here, actors can put money into the bank (this is called savings) and the bank can lend money out to different actors (this is called investment). If the level of savings is equal to the level of investment, then the flow of money doesn't change, and the national income remains at equilibrium (so it is constant over time)

If we add government to the system in addition to a bank, we can call it a governed economy. There difference between a government and a bank is that with a bank, withdrawal and injections of money are voluntary, where as with the government, they are imposed. Taxation is like an imposed version of savings- it takes money out of the economy, while government spending is equivalent to investment, it injects money back into the economy.

If we also add the rest of the world to our economic system, we have an open economy. Here, we can have imports, where domestic consumers purchase foreign goods, and effectively move money out of the economy, and exports where foreign consumers purchase domestic goods and effectively inject money into the economy.

JUST REMEMEBER: for any of these added institutions, as long as all money withdrawals are equal to money injections the GDP is in equilibrium!

----------------------------

GDP - Income

W, R, i, & P all refer to different flows of income- they are the returns for factors of production

W = wages- a return on labour (N)

R = economic rent - a return on land (L)

i = interest - a return on capital (K)

P = economic profits - a return on technology and entrepreneurship (T & E)

GDP - Expenditures

C, I, G, & netX all refer to different flows of expenditure- they are returns for output products (ie: payments for goods and services)

There are four plays in an economy, all of whom must accumulate expenditures

C = Consumption, or expenditures by households

I = Investment, or expenditures by firms

G = Government Expenditure, which is obviously expenditure accumulated by the government

netX = Net exports: in other words, the total number of exports minus the total number of inputs. This is foreign expenditure on domestic goods minus domestic expenditure on foreign goods (X-M).

Y has many many different synonyms. It can refer to:

-national income

-national expenditure

-output

-production

-GDP

-the real thing

-it is a measure of material wealth (the standard of living is the per-capita GDP): this is basically a measure of the material wealth of a nation)

It is NOT, however, a measure of quality of life (money can't necessarily buy happiness).

------------------------

REAL VS. NOMINAL VALUES

Nominal: Actual, current, money, refers to changeable prices and quantities

Real: Constant dollar- here, there are only changes in quantity, while holding the price constant to base year values.

REAL = NOMINAL/PRICE (so real could be the number of cars produced, nominal would be the value of cars produced in 2009, and price would be the price of each car in 2009)

***IN OUR COURSE, WE WILL ALWAYS ASSUME THAT Y IS REAL UNLESS OTHERWISE STATED.

------------------------

OUTPUT GAPS

Potential National Income (Y*) is the maximum achievable output level if all inputs are used at their NORMAL UTILIZATION RATE

Output gap = Y - Y* (actual output level minus potential output level)

If the output gap is negative, then it is a recessionary gap, and the economy is producing at less than its potential

If the output gap is positive, the it is an inflationary gap, and the economy is producing at more than its potential.

-------------------------

THE BUSINESS CYCLE: Changes in Y over real time

4 Stages:

1- Trough (recession/depression)

2- Expansion (boom/recovery)

3- Peak

4- Contraction (slump)

Recessions are downturns in economic growth: two quarters (6 months) of negative growth

Depressions are periods of persistent low growth, high unemployment, and excess capacity

HISTORICALLY, potential output has tripled since 1970, and the output gap is very cyclical (hence business cycles)

Growth varies, but average growth over the last 40 years had been 3.5% per year. Sometimes growth is negative (hence a recession)

WHY DOES NATIONAL INCOME MATTER?

Output gaps concern politicians, because inflation causes high prices which voters do not like, and unemployment also makes voters unhappy. As a result, politicians try to focus on eliminating output gaps.

Economists are more concerned by the potential output. Economic growth is a long term trend we are witnessing: per capita GDP or the standard of living is increasing over time (although this may be deceptive, as standard of living applies only to the average person. In reality, the standard of living may seen reasonable for a country when in reality, there is an enormous wealth gap between the poor and the wealthy).

That's all for today

No comments:

Post a Comment